Context

The increase in the number of cases of Covid-19 in India and the possibility of community transmission led the Government of India to announce a 21- day nationwide lockdown on March 24, 2020. This is expected to have a severe impact on the ability of borrowers to repay their debt during this period. To offset the cascading impact on the economy and the financial health of institutions operating in the financial landscape and to enable borrowers to tide over the immediate impact of the lockdown, the RBI came up with "COVID-19 – Regulatory Package” on March 27, 2020.

Key aspects of the regulatory package

The RBI’s regulatory package allows financial institutions (all commercial banks, including regional rural banks, small finance banks and local area banks, co-operative banks and NBFCs ,including housing finance companies) to grant a moratorium for all EMI payments of certain categories of loans that fall between March 1 and May 31, 2020. The moratorium covers both principal and interest and is applicable for all term loans and working capital facilities.

The repayment schedule for such loans as also the residual tenor, will be shifted across the board by 2-3 months after the moratorium period. Interest shall continue to accrue on the outstanding portion of the loans during the moratorium period. For term loans (including retail loans), there is no mention on when the accrued interest for this period will be collected from borrowers – whether this is immediately due on the first instalment that falls after May 31, amortized over the residual tenor of the facility or due on the maturity of the facility. However, for working capital instruments, it has been clarified that the accrued interest shall be recovered immediately after the completion of the moratorium period.

For the financial institutions, the Board of Directors shall formulate and approve a policy that will be the basis for deciding on the eligibility of loans for the moratorium. The rescheduling of payments, including interest, will not qualify as a default for the purposes of supervisory reporting and reporting to Credit Information Companies (CICs) by the lending institutions. It will also not be treated as concession or change in terms and categorized as restructured loans on the books of the lenders. The asset classification of the loans which are granted relief shall be determined based on revised due dates and the revised repayment schedule.

The package, however, does not cover debt raised from capital market investors and instruments. As such, all NCDs, PTCs (to the extent of collections) and other instruments invested in by Mutual Funds, Insurance Companies, Private Wealth Investors and Family Offices may need to be serviced through this period.

Impact on securitization and direct assignment transactions

Securitization and direct assignment transactions

The RBI has not mentioned anything specific for off-balance sheet transactions. But given that underlying assets managed by the Originators are retail in nature and they will have to allow the moratorium to their end borrowers, it will be difficult to manage differential treatment to the owned and securitized/assigned assets at a contract level.

The collections of the underlying assets will be low in the coming months because of the lockdown and the moratoriums expected to be provided by the Originators, therefore it is prudent to extend the tenor of the securitization and direct assignment transactions.

Without extending the tenor, it is expected that many transactions may see significant early utilisation of credit enhancement, which may prompt rating downgrades in securitization transactions. The investors may also end up with a pool of low rated investments which will impact their overall portfolio and risk weight assets. Therefore, as mentioned earlier investors are incentivised to allow moratorium for the contracts under a securitization or direct assignment transaction in order to ensure orderly servicing of the instruments in the context of a moratorium required / expected in the underlying portfolio.

The Originator’s primary role in this context is that of a servicer and not the lender. Therefore, the Originator will not be able to grant a moratorium on its own. However, transaction documents generally contain a provision enabling the servicer to reschedule any underlying facility or change the terms of any underlying facility with the consent of the purchaser/investor. To implement any moratorium provided pursuant to the RBI COVID-19 Circular and any change in the repayment mechanics, the parties to a securitization or a direct assignment transaction would need to consider instructing the servicers (through the trustee in the case of securitization and directly in case of direct assignment transactions) to apply the moratorium.

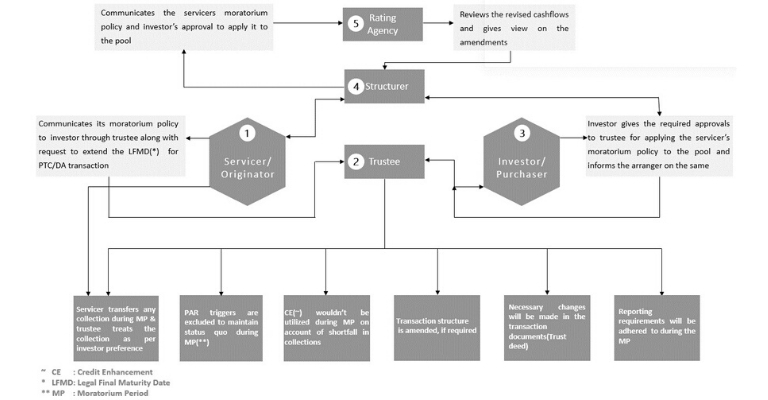

Process of extending moratorium and amending the transaction documents

Below is the suggested process of extending moratorium and amending the transaction documents under a securitization/direct assignment transaction. The flowchart is also shared in the image above.

STEP 1:

Servicer to share its Moratorium Policy (or extract thereof) with Investors (senior and subordinate) through the Trustee along with a request to apply the Moratorium Policy to the assets forming part of PTC and DA transactions and to extend the legal final maturity date (LFMD) in case of PTCs. In certain structures, further consequential changes may be needed.

STEP 2:

Investors to instruct the Trustee to in turn instruct the Servicer to administer its policy for the pool as well.

|

Note 1: As regards such loans (constituting the securitized pool) for which moratorium stands extended, collections, if any, during the moratorium by the servicer will have to be transferred to the trustee and such collections will have to be treated as prepayments and dealt differently in different transactions as per the applicable waterfall mechanism. Accordingly, the Investors shall also instruct the Trustee utilise the such collections towards payments to PTC holders/ Assignee. |

|

Note 2: PAR triggers may not be triggered during the moratorium period as the status quo of the underlying pool will be maintained. |

STEP 3:

Investors to authorise the Trustee to extend legal final maturity date (LFMD) based on the request and their internal approvals.

|

Note 3: CE utilisation during the moratorium will have to be suspended as set out in the table below. Instructions to be given to the Trustee accordingly.

.

|

|

Note 4: Based on the transaction structure, it may have to undergo change. Instructions to be given to the Trustee accordingly. |

STEP 4:

Rating agency will be informed of the servicer’s moratorium policy and investors’ consent to allow moratorium on the underlying pool in line with servicer’s policy. Rating agency will review the revised cashflows and gives its view on the amendments proposed.

STEP 5:

Where necessary, trust deeds will have to be amended in addition to the aforesaid instructions. The trustee will continue to redraw the expected pay-outs schedule as per the terms of the transaction documents and on account of prepayments (due to collections) during the moratorium, disuse of CE during the moratorium, and change in transaction structure, if any. Reporting requirements will continue to be adhered to.

This note only represents our initial views on the current situation as we pay close attention as to how the situation develops. No part of this note be deemed to constitute legal, financial or other advice, recommendation or opinion. Copyright of this note will remain with Northern Arc Capital Ltd. (Formerly known as IFMR Capital Finance Ltd.)